Inside IRS Collections™ | Chapter 3

Lessons from a Former IRS Supervisory Revenue Officer

The Revenue Officer Appointment Letter Is More Than a Meeting Notice

By Brandon Lynch, EA

Founder & Managing Member, Lynx Tax Advisors

Former IRS Supervisory Revenue Officer

Published: July 17, 2026

Estimated Reading Time: 7–8 minutes

Not long ago, a taxpayer’s first personal contact with an IRS Revenue Officer often began with an unexpected knock at the door.

The officer might arrive at the taxpayer’s residence or business without a scheduled appointment. The Revenue Officer had already reviewed the case, but the taxpayer may have had little opportunity to prepare before the conversation began.

That changed in July 2023, when the IRS ended most unannounced Revenue Officer visits. Revenue Officers now generally establish contact by telephone or through an appointment letter before the initial investigative interview. Current procedures ordinarily schedule that first contact at an IRS office or by telephone; a later meeting at the taxpayer’s residence or business may be arranged after contact and safety considerations are addressed.

The change gives taxpayers something they did not always have before:

A defined opportunity to prepare.

But that opportunity often arrives inside a thick envelope filled with unfamiliar documents, warnings, deadlines, and descriptions of what the IRS may do next.

Receiving information and understanding what it means are not the same thing.

One Envelope, Several Different Purposes

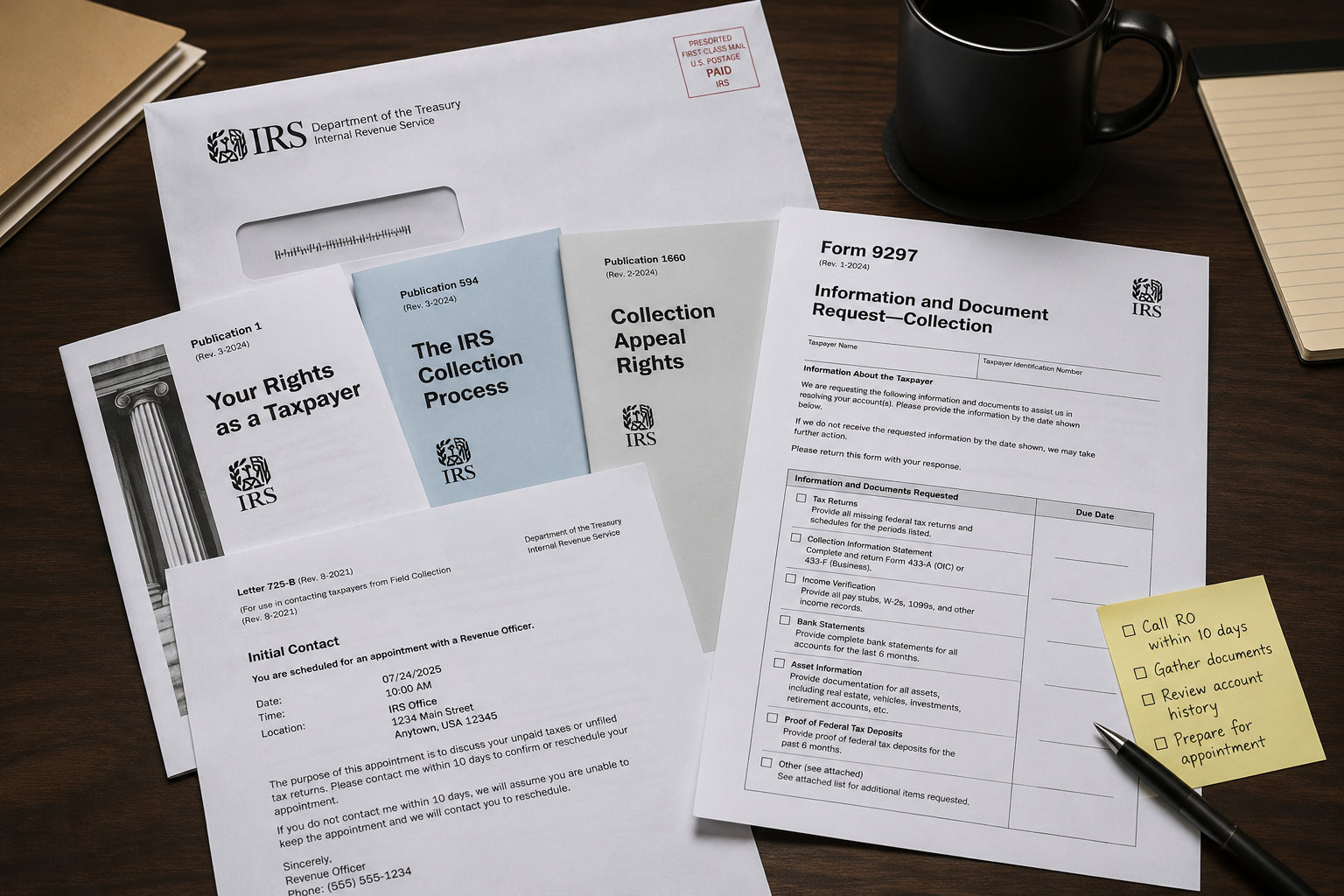

When Letter 725-B schedules the initial investigative interview, the package generally includes:

Publication 1, Your Rights as a Taxpayer

Publication 594, The IRS Collection Process

Publication 1660, Collection Appeal Rights

Form 9297, Information and Document Request—Collection

The letter asks the taxpayer to call the Revenue Officer within ten days to confirm or reschedule the appointment.

To the IRS, each document serves a different purpose.

To the taxpayer, it may all feel like one overwhelming warning.

The packet may discuss liens, levies, seizures, appeal rights, missing returns, financial statements, federal tax deposits, and asset information. A taxpayer may read every page and still not understand which information is general, which request is case-specific, or which deadline could affect an important right.

Reading About Rights Is Not the Same as Knowing What to Do

Publication 1 explains broad taxpayer rights, including representation, privacy, appeal, and a fair and just tax system.

Publication 1660 introduces collection appeal procedures. But terms such as Collection Due Process, Equivalent Hearing, and Collection Appeals Program can be difficult to apply without knowing which notice was issued, which periods it covers, and when it was delivered.

A taxpayer may understand that representation and appeal rights exist without knowing when to exercise them or whether a deadline has already begun.

The information may be on the page. Its significance may not be apparent.

Publication 594 Describes Consequences Beyond a Levy

Publication 594 explains the collection process, including federal tax liens, levies, seizures, summonses, payment arrangements, and collection alternatives.

It also describes a consequence that may immediately concern taxpayers with larger individual balances: passport certification.

For 2026, seriously delinquent tax debt generally means legally enforceable individual federal tax liabilities—including penalties and interest—totaling more than $66,000, where a Notice of Federal Tax Lien has been filed and the related administrative remedies have expired or been exhausted, or a levy has been issued. The IRS may certify that debt to the State Department, which generally will not issue or renew and may revoke a passport after certification.

For someone who travels internationally for work or has family outside the United States, that possibility may feel more immediate than liens or payment plans.

But a Revenue Officer assignment—or even Letter 1058—does not by itself establish that the debt has been certified. Publication 594 explains what can happen. It does not necessarily tell the taxpayer which consequences presently apply.

Form 9297 Is Where the Case Becomes Specific

The publications are largely general.

Form 9297 is individualized.

Depending on the case, it may request past-due returns, a Collection Information Statement, bank records, income and expense verification, asset information, proof of estimated-tax payments or federal tax deposits, and documentation supporting an adjustment or abatement request.

Those requests provide an early view of the Revenue Officer’s case plan.

A request for delinquent returns points toward filing compliance. A request for bank records and asset information signals a financial investigation. A request for current federal tax deposits shows that the officer is examining whether an operating business is remaining current while older employment-tax liabilities remain unpaid.

Frequently, Form 9297 addresses several issues at once.

That makes it one of the most important documents in the packet—and one of the easiest to overlook when the taxpayer is focused on stronger warning language elsewhere.

Information Overload Can Distort Priorities

A taxpayer may spend hours reading about seizures while overlooking a deadline to file missing returns.

Another may focus on preparing a financial statement without realizing that a separate appeal deadline is running.

Someone else may call merely to confirm the appointment and enter a substantive discussion before reviewing the account history or understanding what has been requested.

The taxpayer must separate several documents by purpose while managing the fear and uncertainty of an IRS collection matter.

Most Taxpayers Should Be Prepared for Letter 1058

The original appointment package does not necessarily include Letter 1058, Final Notice—Notice of Intent to Levy and Notice of Your Right to a Hearing.

A qualifying final levy notice may already have been issued by ACS before the account reached the Revenue Officer. The officer is instructed to review the account history and generally not issue another Letter 1058 for liabilities already covered by a qualifying ACS notice.

In other cases, Letter 1058 will be issued during the initial contact meeting.

The IRM states that the notice is usually issued when initial contact is made with a business taxpayer—or a case involving both business and individual liabilities—and the Revenue Officer sets a deadline for specific action. For an individual-only balance-due case, the officer uses discretion and considers the circumstances and compliance history.

During my years in IRS Field Collection, most taxpayers could expect Letter 1058 at the initial meeting unless the facts supported a short opportunity to correct the matter without immediately advancing the case to that stage.

That might occur when a systemic or administrative issue caused the delinquency, the taxpayer could provide a complete remedy promptly, the balance was minimal, current compliance had been restored, and there was little or no prior noncompliance.

That is a practical observation from field experience—not a formal list of published exceptions.

Letter 1058 Is Serious, but It Does Not Always Mean a Levy Has Been Chosen

Taxpayers frequently read Letter 1058 as though it says:

The Revenue Officer has decided to levy my bank account or wages.

That is not necessarily what issuance means.

The officer does not need to identify a specific levy source before issuing the notice. Letter 1058 satisfies an important procedural requirement before most future levy action and gives the taxpayer an opportunity to request an independent Collection Due Process hearing.

When Letter 1058 is issued, the taxpayer generally has thirty days to request a Collection Due Process hearing and preserve the associated right to seek judicial review. The Revenue Officer may continue working with the taxpayer even when a hearing is requested.

The taxpayer may therefore be managing two related processes:

Responding to the Revenue Officer and attempting to resolve the case; and

Deciding whether to preserve independent appeal rights.

Communicating with the Revenue Officer does not replace the need to respond to a separate appeal deadline.

The Appointment Package Is a Preparation Tool

Scheduled contact did not make a Revenue Officer assignment less serious.

The Revenue Officer has already reviewed the account and developed an initial plan. The appointment package begins the taxpayer’s opportunity to understand it.

Before the first substantive interview, the taxpayer should identify:

Which tax periods are assigned

Whether the case involves balances due, unfiled returns, or both

What Form 9297 requests

Which items have specific deadlines

Whether current compliance is an issue

Whether a final levy notice was previously issued

Whether a new appeal period has begun

What facts or records require explanation

The goal is not to avoid responding.

The goal is to respond with an understanding of what each document does and how its deadlines affect the larger case.

Strategy Over Force™

A thick IRS envelope can create the impression that everything must be understood and resolved immediately.

Some taxpayers freeze and do nothing. Others respond quickly without understanding what they are being asked to provide, what rights may be involved, or what the account history already shows.

Neither reaction creates clarity.

The appointment letter schedules the contact. The publications explain general rights and procedures. Form 9297 identifies the immediate requests. Letter 1058, when issued, may begin an important appeal period.

Each document must be read for its own purpose.

Key Takeaway

The Revenue Officer’s first letter is not the beginning of the IRS’s preparation. It is the beginning of the taxpayer’s opportunity to prepare.

Receiving the information is only the first step. The real work is understanding which documents explain, which documents request, which documents warn, and which documents begin deadlines that can affect what happens next.

Because understanding the IRS is more powerful than reacting to it.

Brandon Lynch, EA

Founder & Managing Member, Lynx Tax Advisors

Former IRS Supervisory Revenue Officer

Strategy Over Force™

This article is provided for educational purposes only and does not constitute legal or tax advice. Every taxpayer’s situation is unique and should be evaluated based on its specific facts and circumstances.

© 2026 Lynx Tax Advisors. All rights reserved.

Image credit: AI-generated photo illustration created with OpenAI for Lynx Tax Advisors.

Illustrative image only; not an official IRS document.

Next Chapter

Inside IRS Collections™ | Chapter 4

The First Response Should Be Informed—Not Merely Fast